A sideways look at economics

Take your pick: memento mori (apparently whispered by a slave into the ears of triumphant Roman generals — remember you are mortal): sic transit gloria mundi (so passes the glory of the world, sonorously declared upon the coronation of a new pope); or the phrase quoted in the title of this TFiF, attributed by Wikipedia to ancient Persian scholars, and frequently intoned, usually accompanied with a sigh, by this author. Throughout our history, part of the wisdom of the human species is captured in the idea that everything is temporary. Everything will pass. No matter how bad we feel right now, or how good, it will pass.

If you can meet with Triumph and Disaster, and treat those two impostors just the same…

But does it pass, really? Not in the way you think, perhaps.

The whisper in my ear (in my much more minor triumphs and disasters than those of Roman generals) is provided to me by my phone, and specifically by the photos on it. Every time I pick it up, it flashes up a ‘featured photo’: a moment clipped from my past that causes all the memories of that time to resurface and disrupt the flow of my day. It’s like it’s telling me: don’t get too bound up in stuff that’s happening right now. It will pass. See? That day you’re looking at and thinking about, the one captured in this photo, passed. This one will too.

The photo below is a case in point. It shows my daughter Lucy looking suitably proud of her graduation certificate.

This happened yesterday. But it didn’t: it was taken in September 2019, BC (Before COVID). Before everything changed. A different world. I get a jolt when I think about it — about how different everything felt back then. Sure, that day passed, and this one will too. But some of the things that happened between then and now will never really pass.

The last two years have fundamentally changed what life is like for the foreseeable future. In fact, that process, of fundamental shifts, for better or for worse, sometimes large, sometimes small, is happening constantly. Those shifts don’t go away. What changes is how we feel about them.

This time of year whispers in all our ears the echoes of past traumas like the world wars — just reflect on the impact they must have had on the people who lived through them: the loss they created that would never be restored. On the other side of the ledger, think about the impact that the invention of penicillin had on people’s lives, on what was considered ‘normal’ before and after that moment in time. Those effects (and countless, innumerable others) never passed. They are with us to this day. As are the impacts, for example, of Julius Caesar’s rise and fall all that time ago, despite the whispers of his slave.

What is normal now is the accumulation of all those historic shifts, for better or worse, all built into our current lived experience.

But (and here’s the pivot) how we feel reflects how we stand in relation to that constantly shifting ‘normal’. Some things don’t really ‘pass’ at all: they become normal.

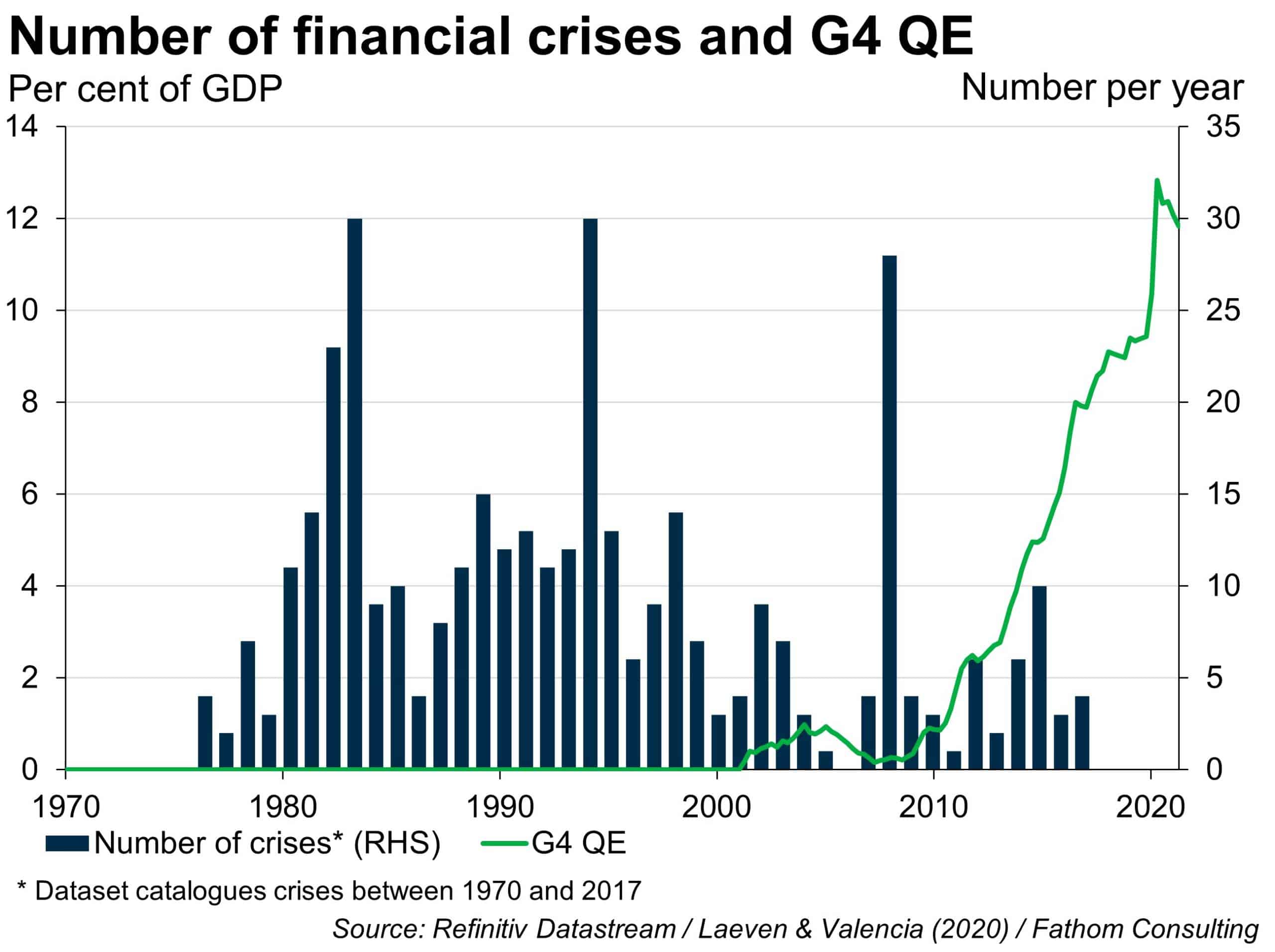

There are many resonances of this idea in our work. One example: at Fathom we created and maintain a global Financial Vulnerability Indicator (FVI) which captures the probability of three kinds of financial crisis in every country over time. The kind of thing that goes into our estimate of the likelihood of a sovereign crisis, for example, is the ratio of government debt to GDP. The higher it is, the higher the likelihood of a sovereign crisis. Makes sense, right?

Well, not exactly.

The first version of the FVI (1.0) included exactly that measure. It was trained on data up to and including the Great Financial Crisis (GFC) across many economies. We found, at that time, that the ratio of government debt to GDP at each point in time helped to explain the incidence of sovereign crisis a few years later. Scroll forward ten years, however, and that’s no longer the case. The ratio of government debt to GDP has increased dramatically in most countries since the GFC, but the frequency of sovereign crises has fallen. The relationship we found in FVI 1.0 no longer exists. We can all see why: after the GFC, central banks around the world introduced quantitative easing (QE) as an adjunct to conventional monetary policy, on an absolutely massive scale.

QE was introduced initially as a temporary measure! And this, too, shall pass. Twelve years later, there is no sign of QE ‘passing’: it is part of the new normal and will remain so for the foreseeable future. (Even if, at some point, the quantity might stop growing.) The introduction of QE changed the relationship between government debt and sovereign crises once and for all. A model that keeps on and on ringing alarm bells because of the build-up of sovereign debt would be no use at all.

FVI 3.0 takes a different approach. We now find that it’s how the ratio of government debt to GDP stands in relation to its ‘trend’ that matters for the likelihood of sovereign crisis. Higher debt ratios are normal. It’s a question of how close to normal any given country is. The trend is the accumulation of a series of (recently positive) steps up in the ratio of debt to GDP. Those changes have not ‘passed’, except in the sense that they’ve passed into the trend and out of our immediate consideration when we’re thinking about financial vulnerability. Higher debt ratios are normal. It’s now a question of how close to normal any given country is.

Part of me rebels at that thought: what, you mean you just FORGET about the long-term build-up in the level of government debt? That markets just stop worrying about it?

How about inflation? If the current burst of inflation proves not to be transitory, should we just forget about the inflation target and shift to a new normal, a higher target, perhaps? Think of all the hours that have been spent poring over the inflation data, fretting about small deviations from the target and so on: all of that will just become water under the bridge, forgotten?

And what about house prices? If the ratio of house prices to income has shifted up, should we just forget that it used to be much lower? Those quaint old days when young professional couples could afford to buy a house will vanish into history and into half-remembered anecdotes, like when my grandparents used to tell me about horses pulling carriages into the City of London.

And I feel the same about COVID. What, you mean I just have to accept that COVID has changed the world forever? I’m not ready to accept that! I’m not ready to let the pre-COVID normal pass. I want it back.

But it has passed. That’s the jolt I get every time a picture pops up on my phone that takes me back to that time. The world has changed and it’s not changing back. This is normal now.

That’s the sense in which everything shall pass. Some events are genuinely temporary, ephemeral. Others have permanent effects, but those effects will be absorbed into what we consider normal — so yesterday’s normal is not the same as today’s. We just have to get over it. That’s our memento mori: remember that what’s normal is constantly changing.