More support for zero-emission flight, please

The need for more and broader support for zero-emission flight is a preliminary conclusion from Fathom’s recent research to compare the costs, benefits and challenges of different ways to decarbonise European aviation. We also examined how investing in aviation decarbonisation can support wider European policy objectives, such as creating jobs, increasing economic productivity and enhancing energy security.

![]()

Brian Davidson

Head of Climate Economics

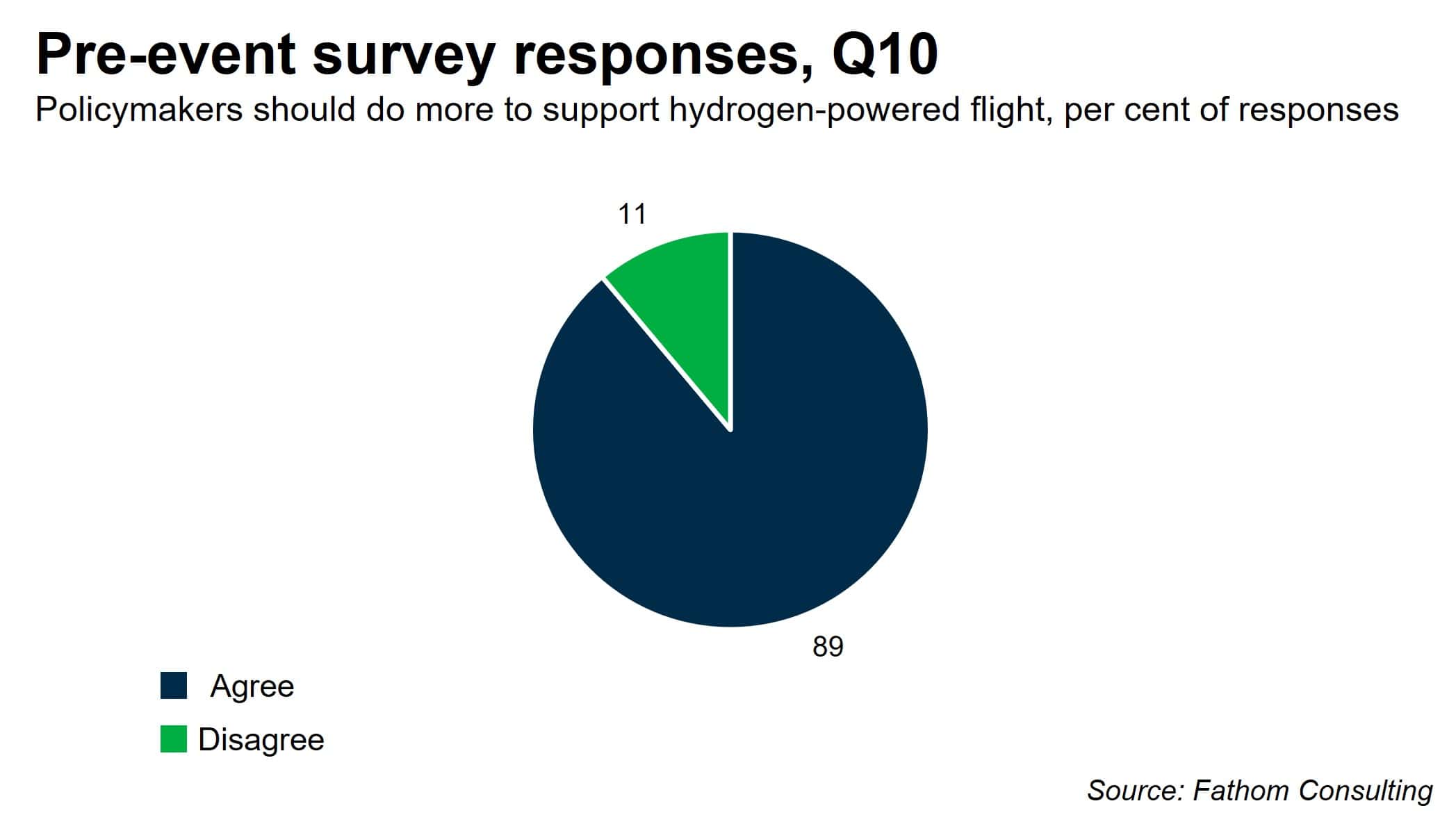

Participants pointed to an imbalance in current policy in both the EU and UK, in which Sustainable Aviation Fuel (SAF) is given attention, but not zero-emission flight (ZEF), or flight powered by hydrogen. Since in our view ZEF will be needed, policymakers should do more to support it, via regulations (such as a ZEF mandate) and by supporting ZEF-related R&D. Many participants agreed, while adding that the private sector too should do a lot more to support ZEF. This does not mean there is no role for SAF. In fact, in a pre-event survey, nearly 90% of respondents replied that SAFs do have an important role to play in decarbonising aviation (full results can be seen here).

Read on for details of our presentation and the discussion that followed. The slides that were presented on the day are accessible here, and more information about the project can be accessed here.

Extreme scenarios give us important information

To consider the merits of SAF and ZEF, we look at scenarios in which all European aviation by 2050 is decarbonised using a single method (different types of either SAF or ZEF). Several participants questioned our use of these 100% scenarios, since very few people expect any one solution to account for all the decarbonisation that will happen by 2050. We aren’t suggesting that these scenarios reflect real-world outcomes. But they are helpful to frame the problem, and to understand the trade-offs between the costs, benefits and limitations of each method. Ultimately, by understanding things in isolation, we can see things with more clarity, which will help us understand what a more suitable mix might look like in 2050, and why. Our final analysis will certainly consider a more balanced mix between the various options.

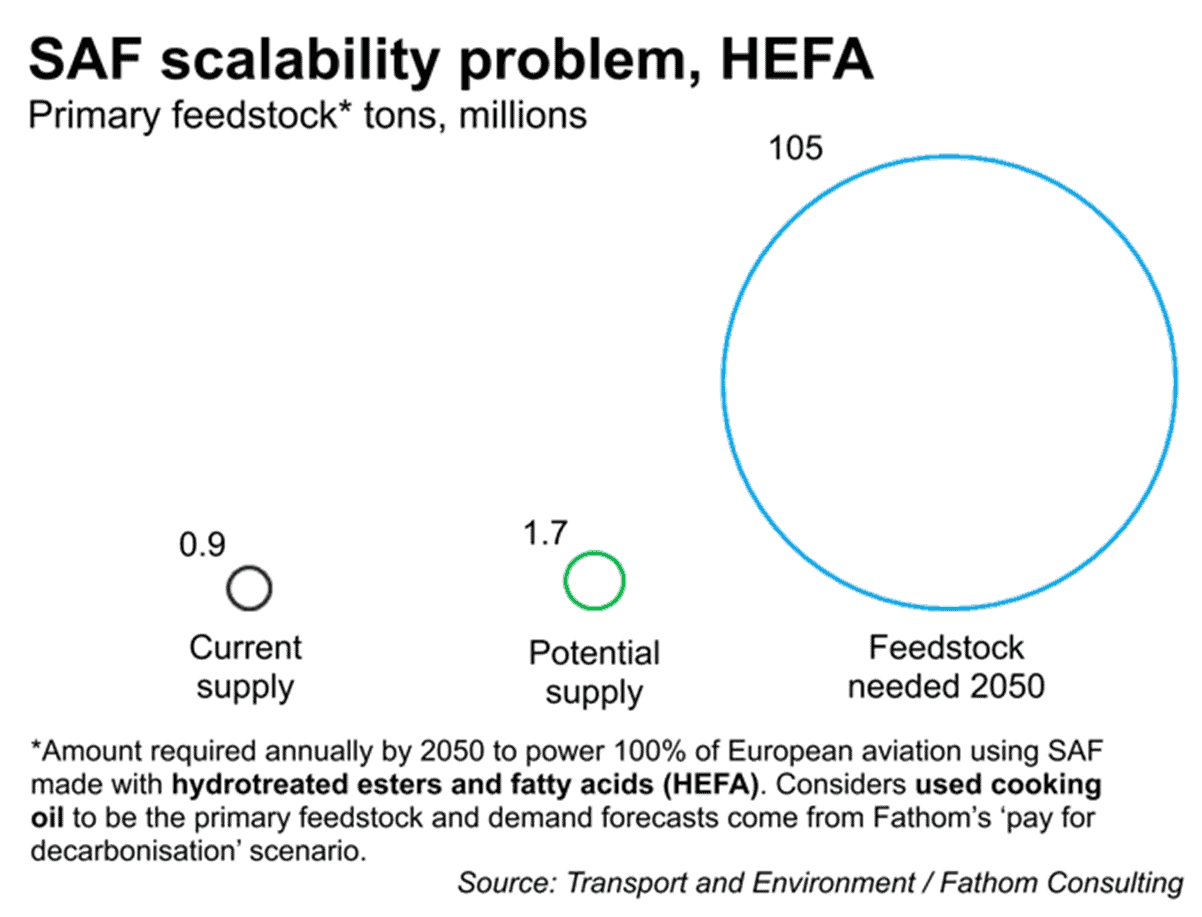

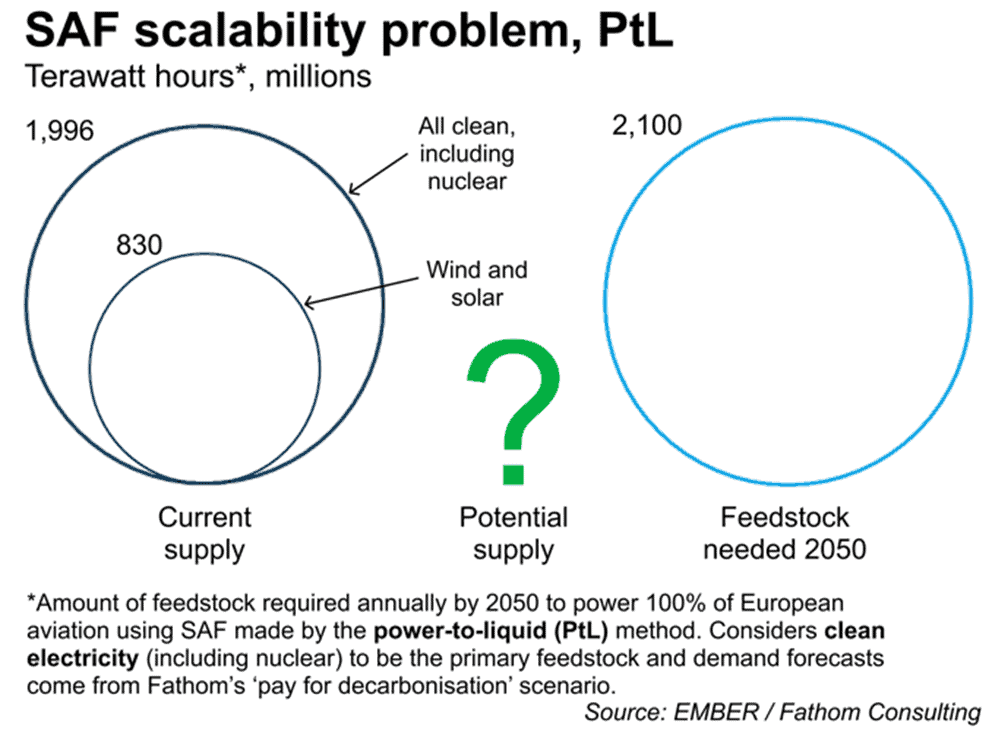

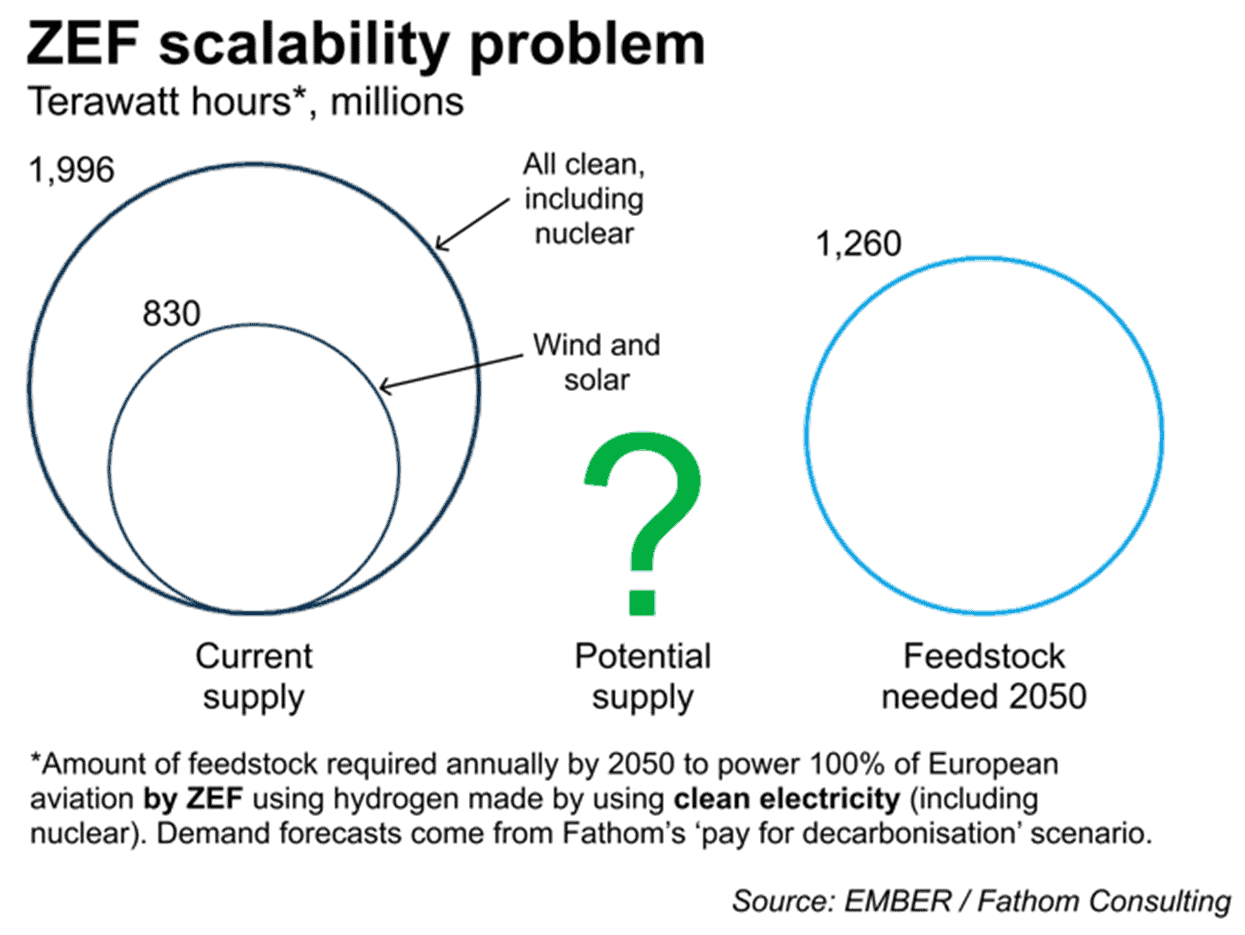

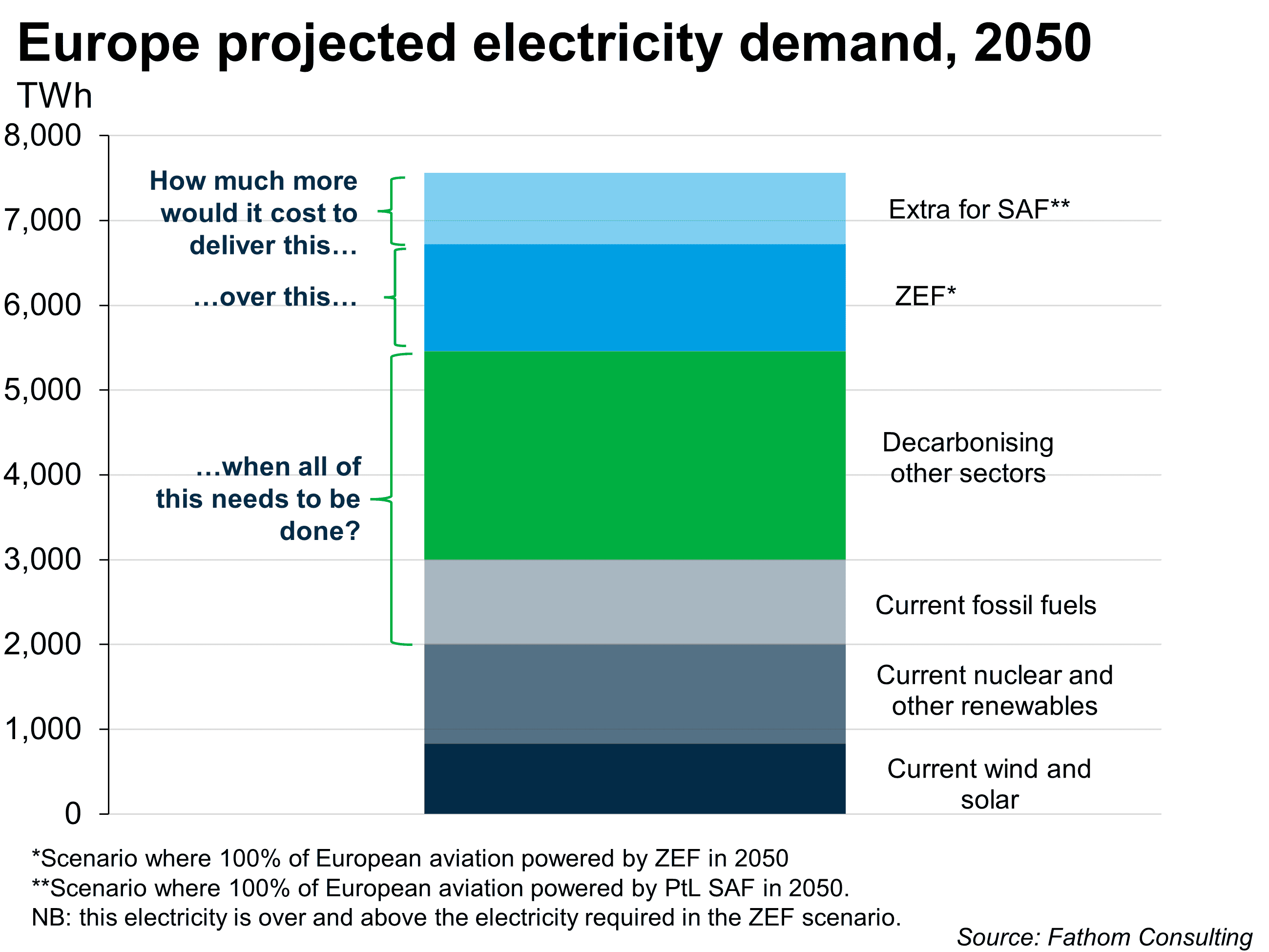

The charts below show how much of each primary feedstock would be needed in 2050 to fully decarbonise European aviation using different methods; and compare this to the current supply of that feedstock and potential supply in 2050.

These charts demonstrate that to decarbonise aviation using only PtL SAF would demand the total current supply of clean energy, while doing so using ZEF would require more than 60% of all clean energy. As we discuss below, there are other, competing claims on that supply, and these claims are set to increase dramatically. The upshot is that to decarbonise aviation using either of these methods, a lot more clean electricity will be needed.

There is clearly a role for ZEF in decarbonising aviation

Another early, and clear, conclusion from our work is that due to the scalability challenges with various forms of SAF, ZEF clearly has a role in decarbonising aviation. While the size of this role is unclear at this stage of our analysis, the fact that it has a role is significant. By implication, this raises the question why there are SAF mandates in both the EU and UK, but no ZEF mandates. One participant commented that they found our framing, using 100% scenarios, useful to better understand the fundamentals and to shine a light on this policy imbalance. Participants appeared to agree with this finding, as 89% of respondents in our pre-event survey said that they thought policymakers should do more to support hydrogen-powered flight.

R&D has numerous benefits

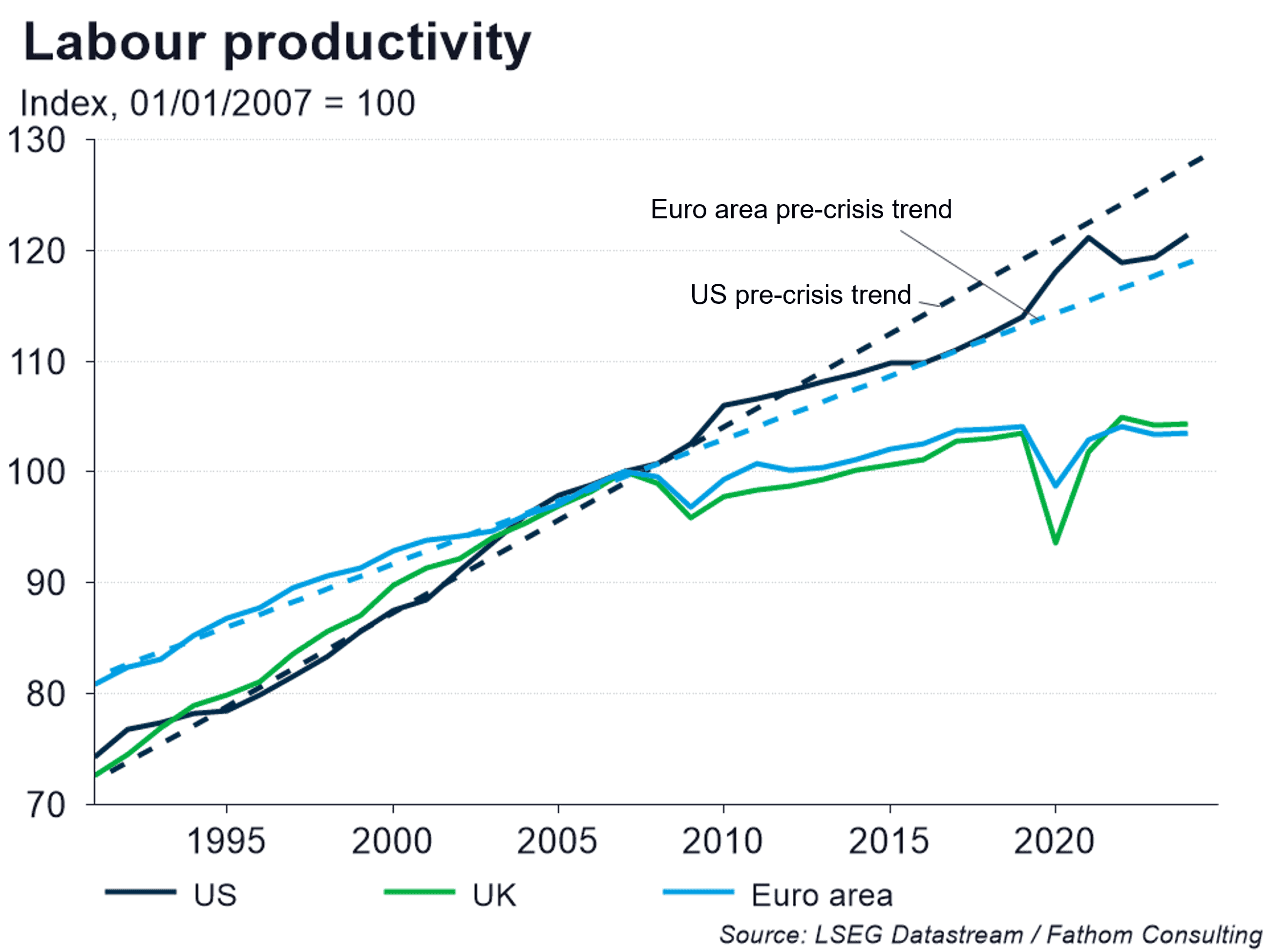

Our presentation highlighted how European economic productivity has stalled relative to its pre-2008 trend, and relative to productivity in the US. We described possible reasons for this and how Europe could start to close this productivity gap by taking a lead on decarbonisation, especially through ZEF. Previous Fathom research has shown that aerospace R&D has big, positive spillovers to other sectors of the economy, with large economic and social benefits; and that countries that do more R&D tend to be more productive.

One participant asked how much R&D for ZEF could be supported by governments, since public funds are tight. We answered that there is a strong case to be made for government investment, due to the positive spillovers which themselves would generate tax receipts and help to pay for this R&D; not to mention the environmental benefits. More generally, Fathom’s view on this is that ‘tight funds’ should apply to current spending commitments (wages and salaries, transfers and public procurement), but not to investment opportunities, where a different constraint applies. For investment, if the expected returns exceed the cost of finance, then it makes sense to invest more. This would certainly apply to R&D.

We also noted that it would be helpful to invoke the attitude taken to COVID vaccines, which were rolled out in a much shorter timeframe than anybody had thought possible, with support from policy and taxpayers. One participant mentioned that it was possible with vaccines because many were on board with how “important” that was to society. We questioned why this is not the case for decarbonising aviation and the climate crisis more generally. We also pointed out that the decision to pursue COVID vaccines was made with eyes wide open with respect to the costs involved, and that despite the likely failure of many attempts the returns were judged sufficient to justify those costs and those risks. One participant suggested that it will be important for our analysis to outline clearly why ZEF is important, not only to aviation and air passengers but to broader European society, and what the consequences could look like from failing to support ZEF.

Several participants noted that it was not just the government that needed to contribute money to ZEF R&D, but that larger players in the aerospace industry needed to do this too. We agreed, while noting from our previous research that R&D tends to ‘crowd in’ more private finance than other types of government spending or investment, and that in the case of aerospace this ratio is 3:1. One participant suggested that investors should exert more pressure on the big aerospace players to do more, and suggested that the EU’s green taxonomy could be useful in this respect. One participant noted how the industry itself will suffer from the physical effects of climate change, such as through damage to aircraft and airport infrastructure, and that industry stakeholders should be reminded of this to be spurred into action. We mentioned how governments had the power to curb flying, and that this risk should be heeded by the industry too, especially since aviation’s share of economy-wide emissions are set to rise.

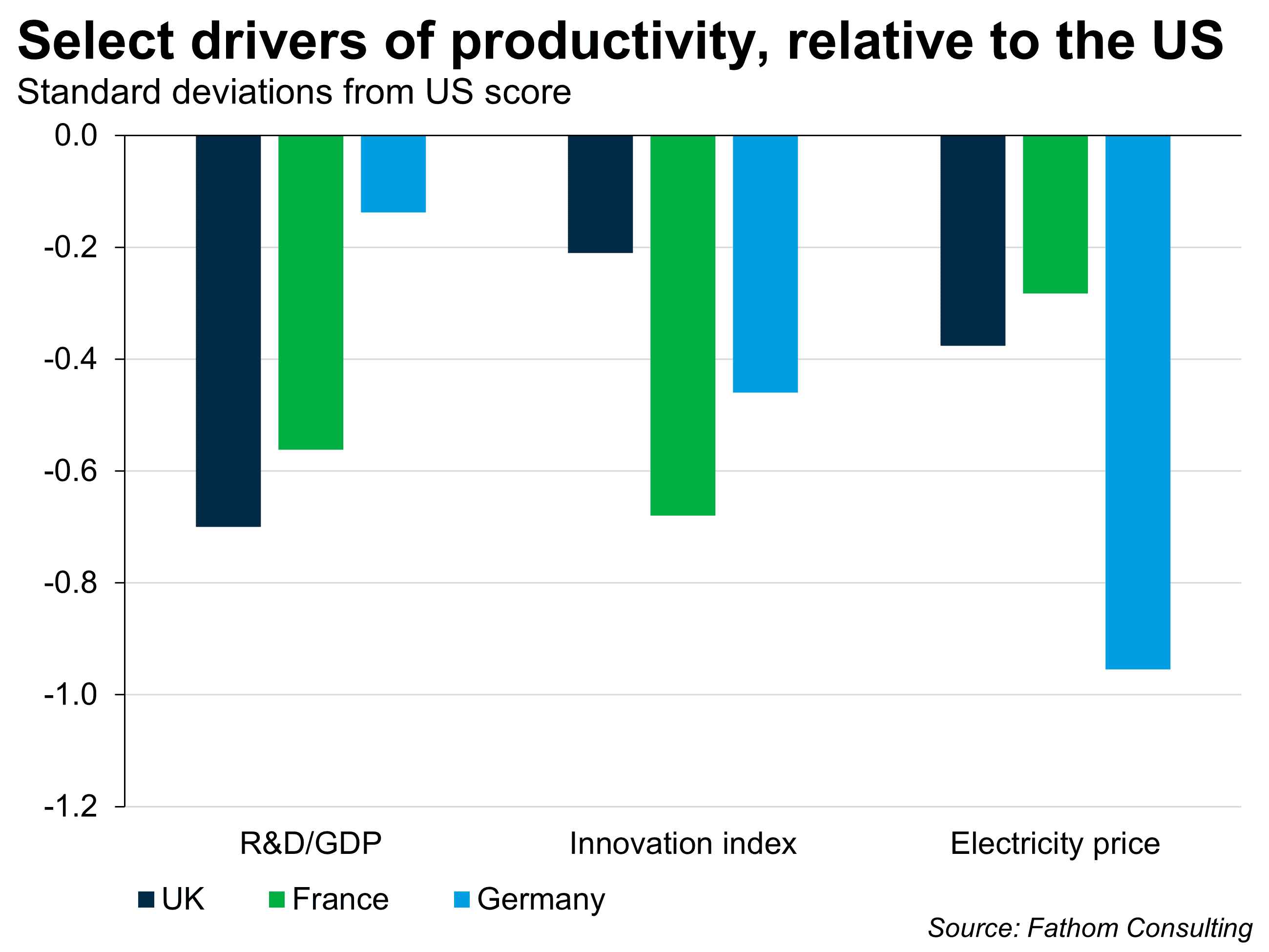

One participant noted that Europe has a poor track record in commercialising its R&D. This is indeed true, and something that Mario Draghi discussed in his recent paper on EU competitiveness.[1] It is also true, though, that Europe does less R&D than the US as a share of GDP, as demonstrated by the chart below. It is worth pointing out that R&D in ZEF has a relatively clear and defined route to commercialisation; and that from a wider perspective, even if that R&D is not commercialised in Europe, the act of conducting it will still benefit Europe through its positive climate impact and its spillovers to other economic sectors.

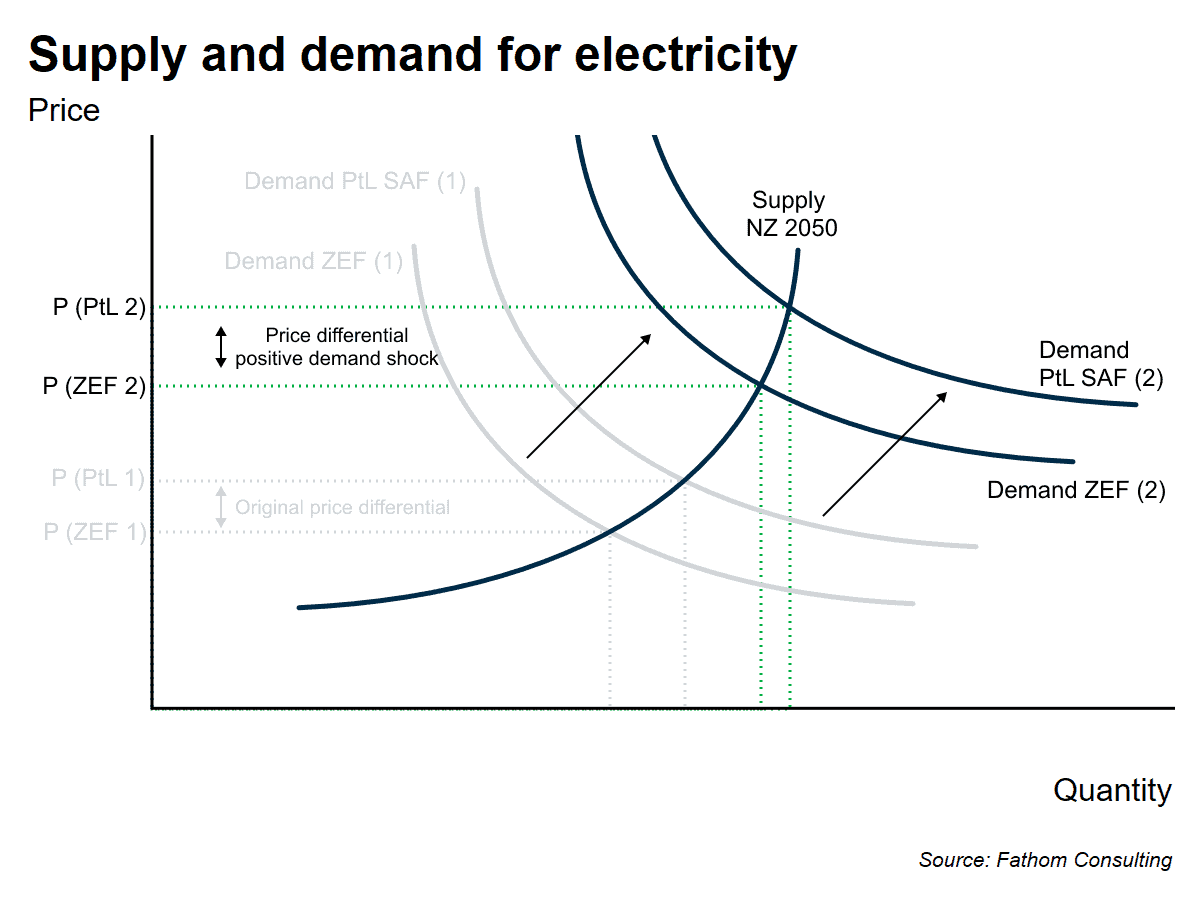

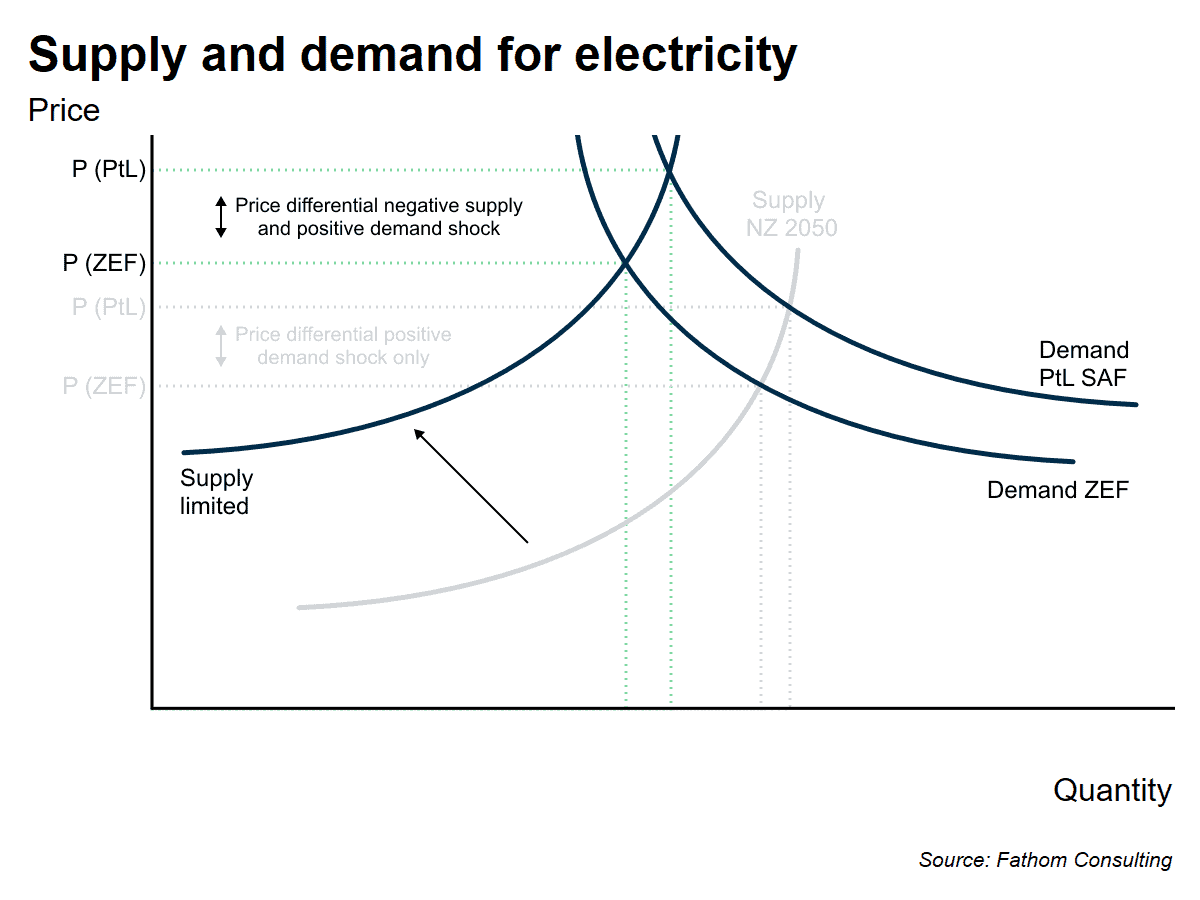

Framing the issue using supply and demand curves

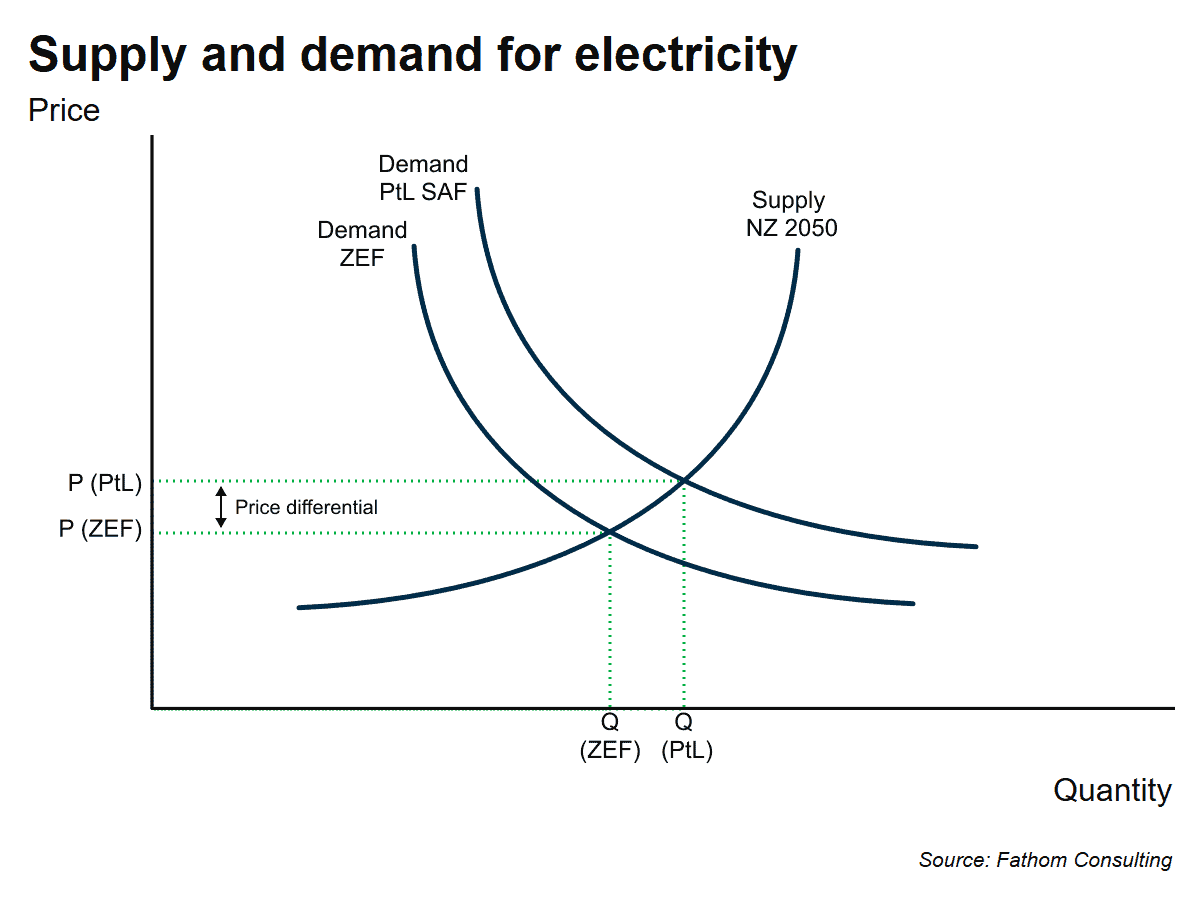

We showed how availability of feedstock is a constraint for different types of SAF. PtL (power-to-liquid) SAF, sometimes called eSAF and made by combining hydrogen with CO2, may be the most scalable type of SAF. We noted how producing the hydrogen and capturing the CO2 using direct air capture (DAC) would both require very large amounts of electricity. Decarbonising aviation using ZEF would also require a very large amount of electricity, although about 40% less. We said that this electricity differential needs to be considered in the context of the demand for clean electricity — demand that is already likely to double as a result of having to fully decarbonise the existing electricity mix, decarbonise other sectors and also meet rising demand from AI.

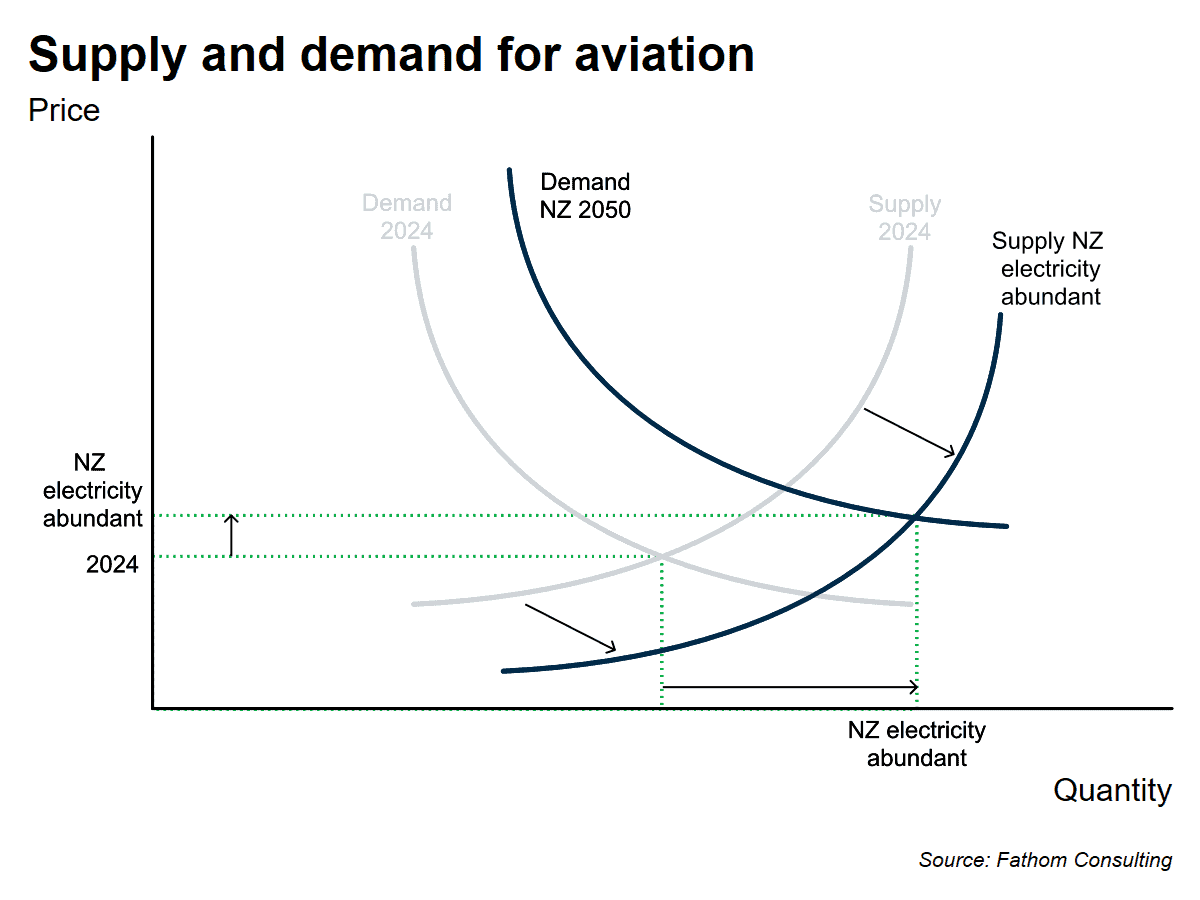

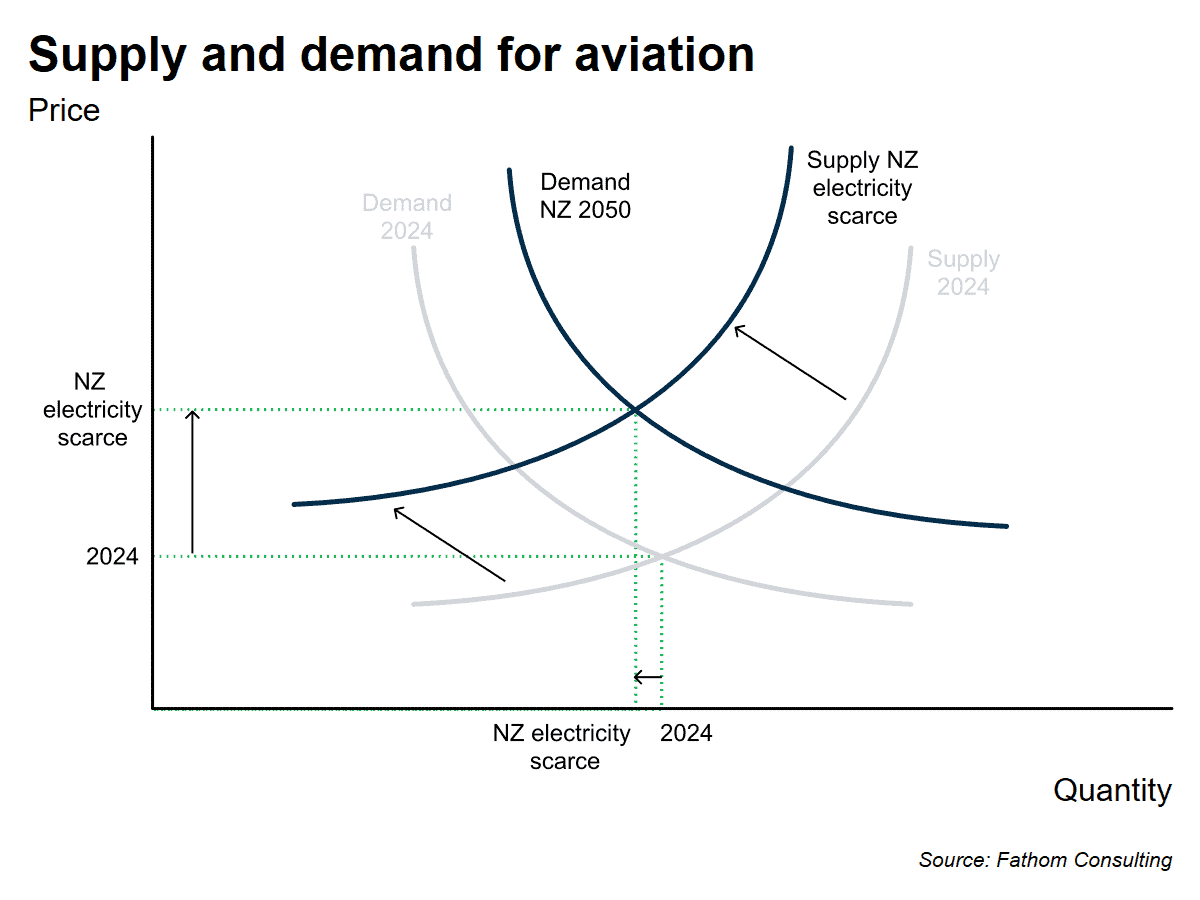

The additional cost of electricity in scenarios where PtL SAF is prioritised over ZEF will depend on how the supply of electricity evolves to meet rising demand. At the webinar we used illustrative supply and demand curves to show how this electricity price differential will depend on supply and demand dynamics; and also how electricity prices will affect supply and demand for decarbonised aviation, the quantity of flights taken and the cost of those flights. One clear takeaway is that abundant, clean electricity will be essential to decarbonise aviation using PtL SAF or ZEF, and that cheaper electricity will make it cheaper to fly.

We also showed how a limited supply of electricity would increase aviation costs and reduce the number of flights taken. One participant noted that using supply and demand curves was an interesting and different way to approach this issue. They added that these would change if foreign-supplied electricity, SAF or hydrogen were used in European aviation; and that the costs of transporting SAF are currently considerably lower than the costs of transporting hydrogen, which could affect our calculations.

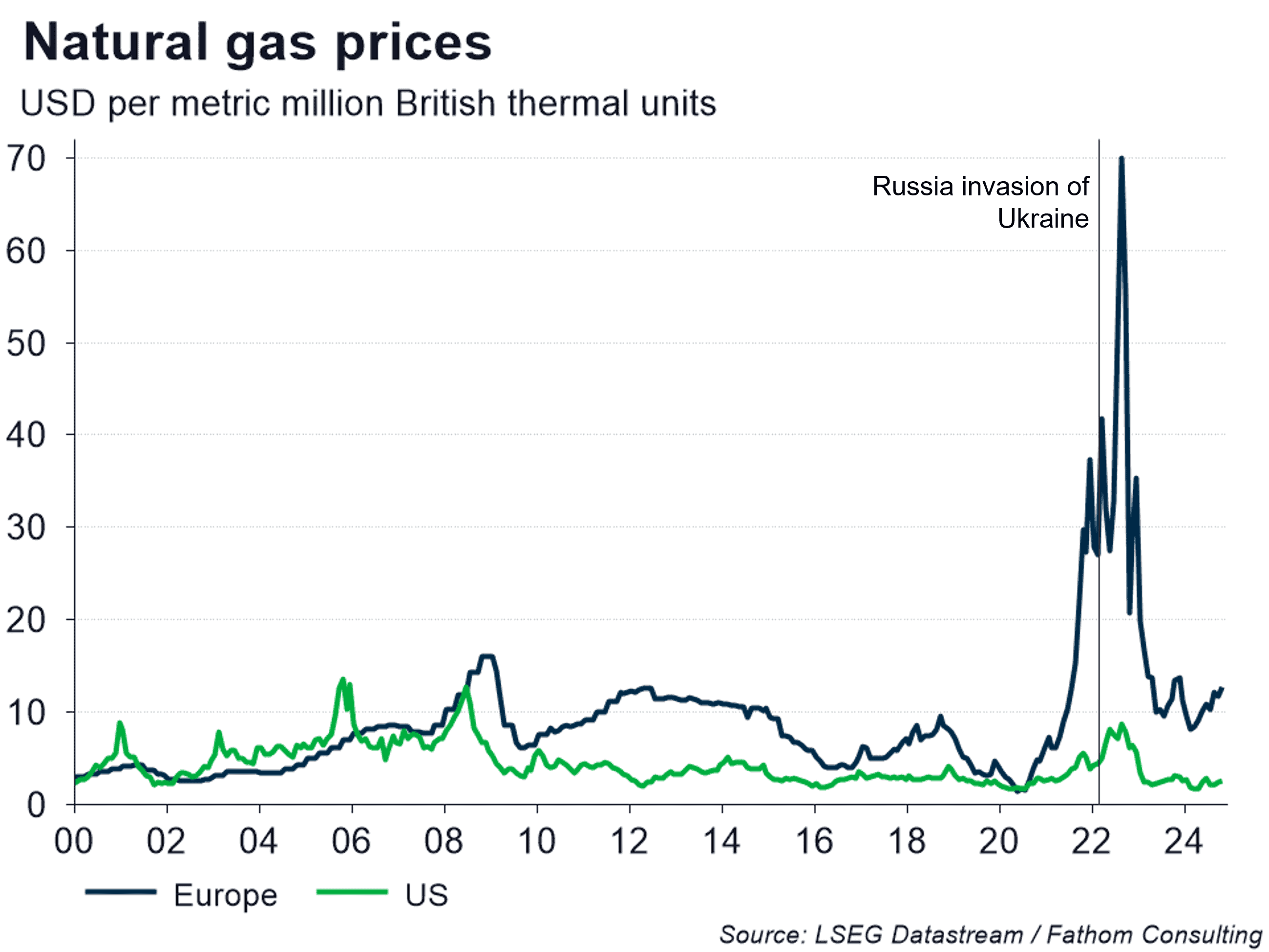

Energy costs and energy security

The fact that these supply and demand curves will change if energy is imported is a good point, which we will consider in our analysis. That said, there will be a lot of uncertainty about foreign supply of and demand for electricity, SAF and hydrogen, which will affect the price differential, and all of this will need to be considered. In our presentation we also showed that it is in Europe’s interests to have greater energy security (the chart below demonstrates the risks attached to insecure energy supply). Europe does not want to go from a dependency on imported gas to a dependency on imported SAF, hydrogen or electricity. The benefits of cheaper foreign energy will need to be carefully weighed against the disadvantages of greater energy insecurity.

DACCS and DACCU

During our presentation we raised the issue of direct air capture (DAC) and whether its use would be allowed in decarbonising aviation. In future, it is possible that policymakers will consider DAC essential to reduce the large stock of CO2 in the atmosphere, and that any DAC should be used to capture carbon and store it underground (DACCS) rather than as a feedstock for SAF (DACCU). We noted that this risk alone pointed to a role for ZEF in aviation’s decarbonisation mix.

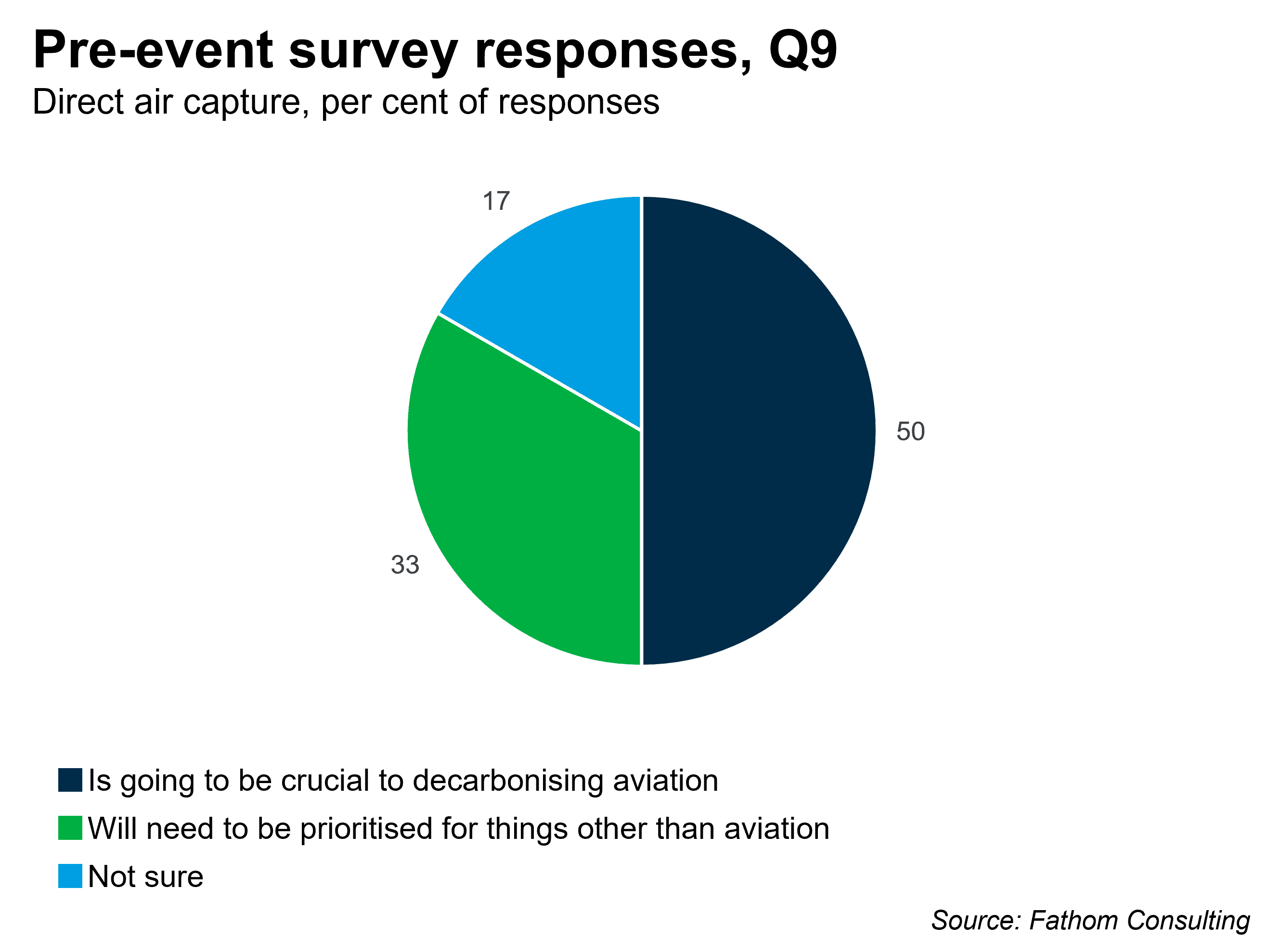

We asked participants if they knew about the potential to scale DAC. One participant shared the IEA’s projections for global CO2 capture by DAC and by biomass in its Net Zero scenario. A range of other studies which may shed light on this question were also shared. One participant raised this issue during the Q&A, expressing concern about the availability of CO2 and its important role as a feedstock for PtL SAF. In our pre-event survey, we asked whether DAC has a role to play in decarbonising aviation or whether it should be prioritised for other things. Half of all respondents replied that DAC will need to be prioritised for things other than aviation.

Other costs and benefits

The relative costs and benefits of SAF and ZEF go beyond electricity. Other considerations include R&D, which is scored as a cost in the short term, but which generates benefits that are usually held to far outweigh that cost in the long term. They include energy security; and also tech leadership and the soft-power benefits that brings. One participant, while recognising the importance of electricity, noted how focusing on other costs and benefits would be very important.

Other costs include system changes (new ways of refuelling planes, obtaining safety certifications and so on); new infrastructure; scrapping of existing infrastructure and/or aircraft; the social cost of carbon (or other greenhouse gases and contrails); and the supply risks associated with feedstocks, especially CO2.

One participant said that it was not feasible to assume that ZEF will cover all flights, since hydrogen-powered aircraft will require a lot of new infrastructure at airports, which will most likely not be feasible or efficient everywhere, reducing the potential for ZEF Another participant noted how ZEF had an advantage in terms of air quality and reduced noise.

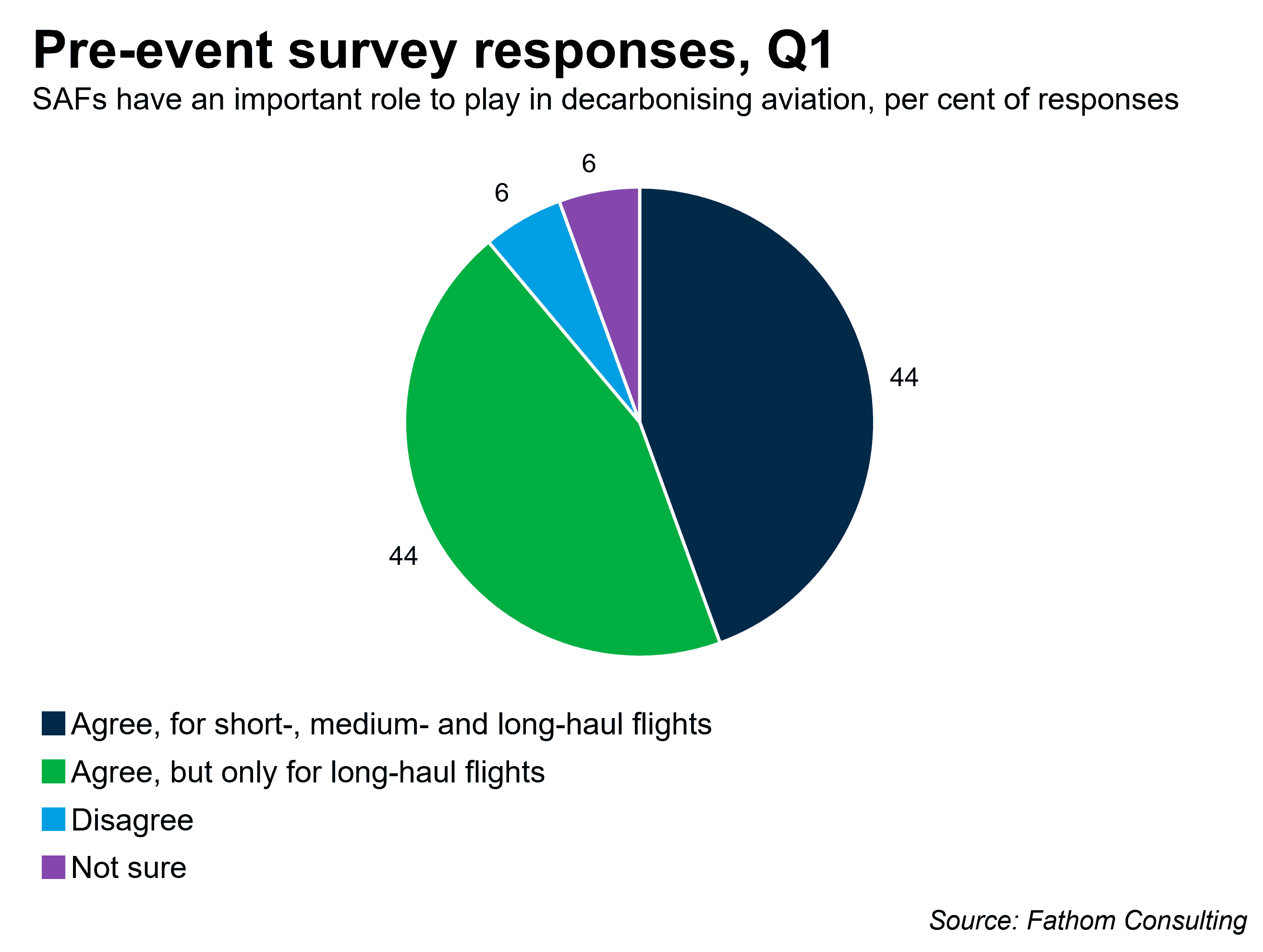

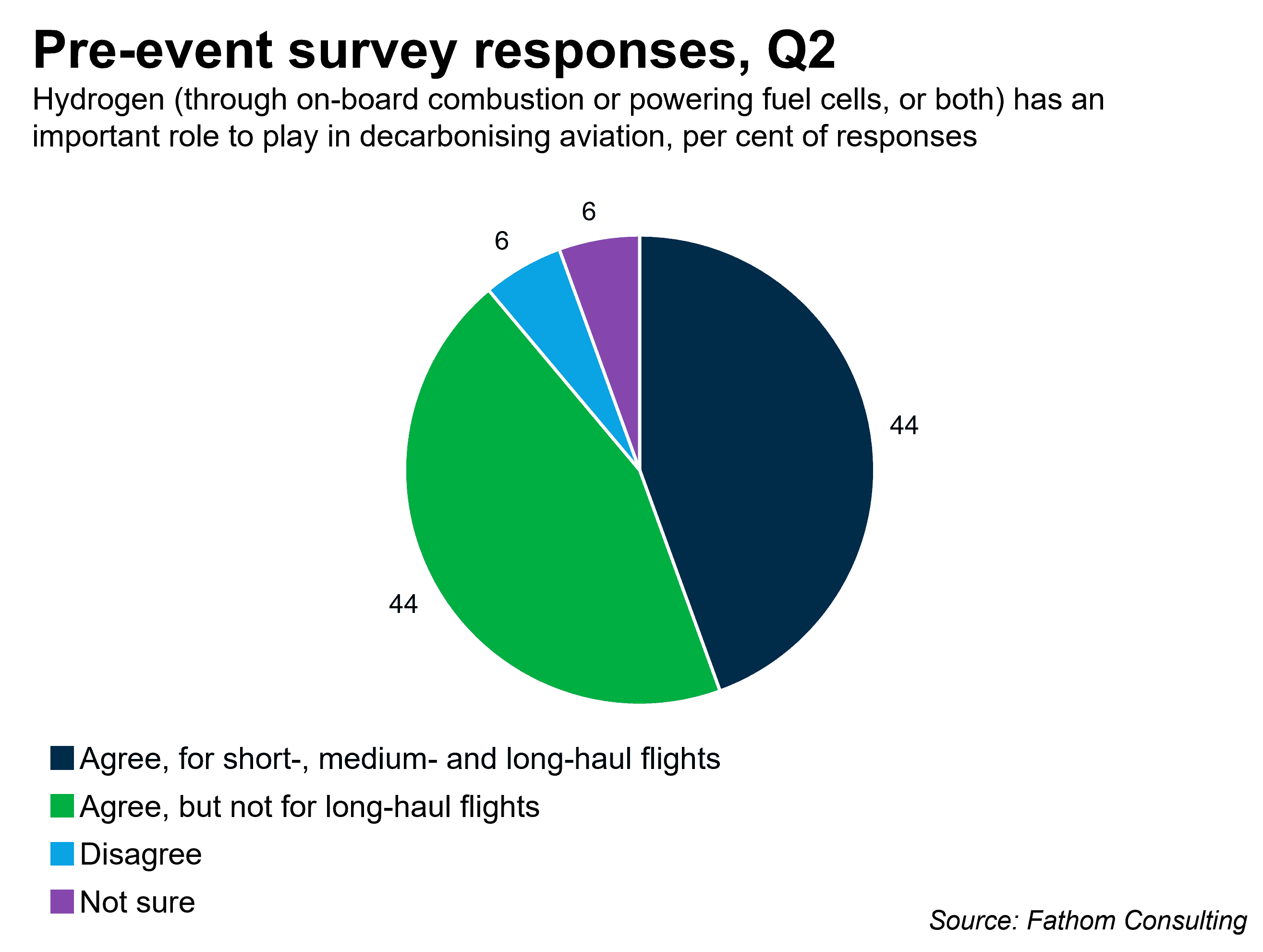

There was a discussion around infrastructure, and we noted that our research has shown that the fiscal multipliers on government-backed infrastructure spending were far inferior to those on government-backed R&D spending. One participant commented, however, that certain infrastructure spending was needed to support R&D (for example, to make hydrogen available for testing new aircraft). Some participants noted how the cost-benefit analysis between SAF and ZEF would differ between short-haul and long-haul flights. Indeed, in our pre-event survey, 44% of respondents said they believed that SAF had an important role to play in decarbonising aviation, but only for long-haul flights. Similarly, 44% of respondents said that they thought hydrogen had an important role to play in decarbonising aviation, but not for long-haul flights.

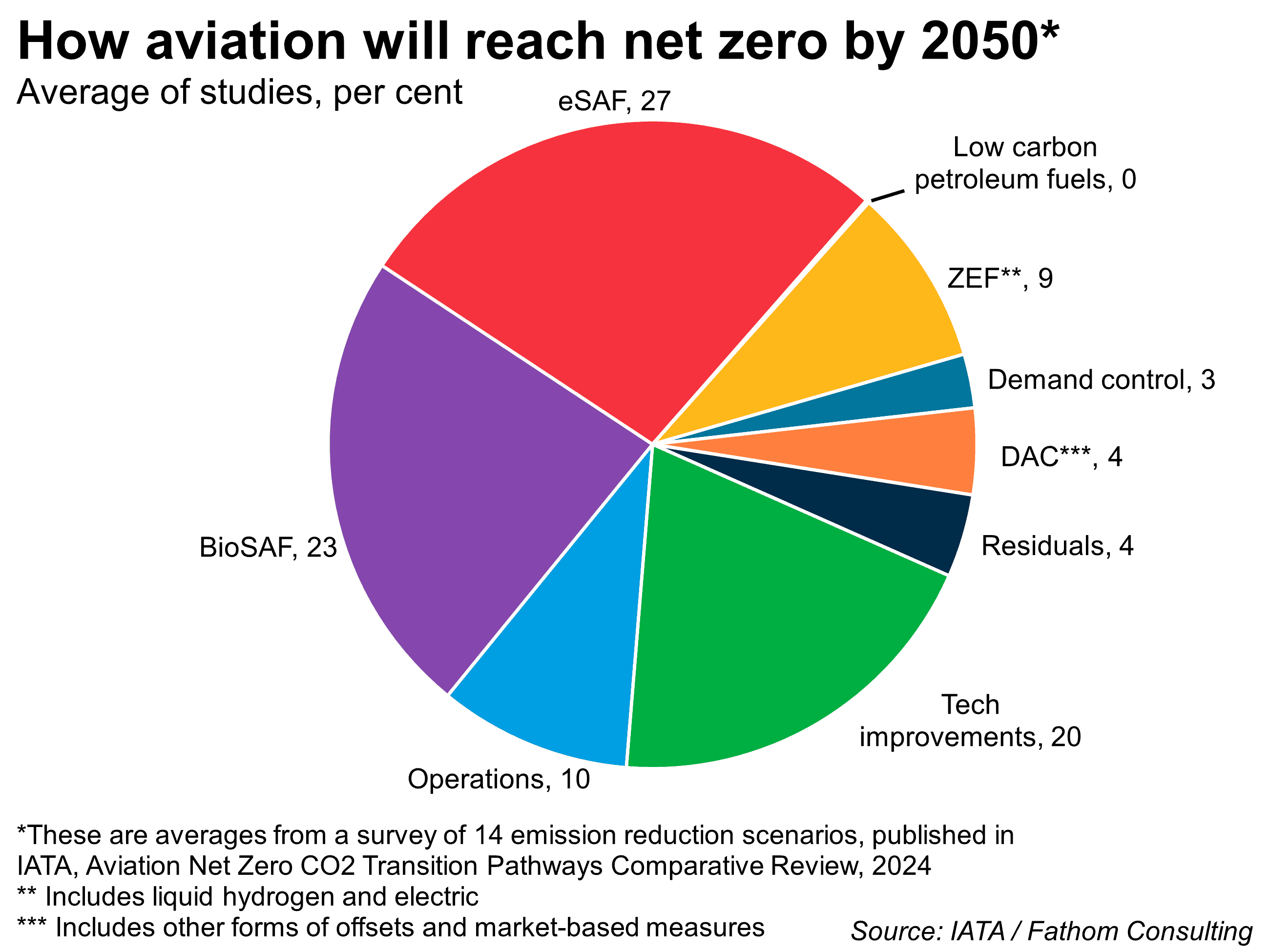

Representativeness of IATA study

Participants questioned our inclusion of an IATA study in our presentation, in which 14 different aviation decarbonisation pathways were considered. Specifically, these studies each attributed the share of decarbonisation that they expected to come from various fuel sources (including SAF and ZEF) and other factors. We showed the average contribution of each of these across the 14 studies. Some participants said that this summary was not a fair representation of the work that has been done on this subject, and that most of the studies in question seemed to be linked to the airline industry and did not reflect a consensus on this issue. We agreed that these were fair comments. These studies, on average, showed a limited role for ZEF in 2050.

Our intention was to demonstrate that this is a prevailing view among this cohort of stakeholders; indeed, it seems to be the prevailing view among European policymakers too, given the existence of SAF mandates (i.e. a requirement that 70% of the fuel used to power an aircraft fuelled at European airports in 2050 would need to be SAF), but no ZEF mandates. As the rest of the material in our presentation showed, it seems to us that ZEF will need to play a role due to the scalability issues associated with SAF, and that current policy (which prioritises SAF over ZEF) should be changed to accommodate this. The policy imbalance appears to ignore the risks of SAF (mainly, but not exclusively, linked to feedstock constraints), and possibly the benefits of ZEF too. We hope that our work can lead to a more balanced and informed debate on this complex, but critical – and still poorly understood – issue.

Next steps

This webinar marked an important milestone in our work on this project. We intend to present our full findings in Spring 2025, and the project runs until June. While we are confident in our initial conclusions, and in the data and analysis done so far, and have cross-referenced our findings with the literature and across different data sources, the results that we have presented here are preliminary. We wanted this webinar to be an interactive session, and we regret that we were not able to invite more stakeholders to the discussion. We believe it is critical to share these issues and debate them in a rigorous way; and we therefore welcome thoughts and feedback on these issues from any interested stakeholders, especially if you think we are missing something, or have misrepresented participants’ views, or have got something wrong. Feel free to share this material, and information about our study, with those who might be interested. The event was held under the Chatham House Rule, meaning that we, and participants, can publicly discuss what was said, but should not attribute those comments to any individual participant. We also noted at the outset that participants’ views reflected their own opinions and not those of their employer.

[1] “The innovation pipeline in the EU is also weaker at the next stage of commercialising fundamental research.” Mario Draghi (2024), ‘The future of European Competitiveness,’ European Commission

Fathom is a world-leading consultancy specialising in the global economy, geopolitics and financial markets. One of our core focuses is climate-related research. We provide clear analysis and advice on the energy transition, and the economics of climate change, to assist policymakers, strategists and investors.

The European Climate Foundation (ECF) is a major philanthropic initiative working to help tackle the climate crisis by fostering the transition to a net-zero emission society at the national, European and global level. It supports over 700 partner organisations to carry out activities that drive urgent and ambitious policy in support of the objectives of the Paris Agreement, contribute to the public debate on climate action and help deliver a socially responsible transition to a net-zero economy and sustainable society in Europe and around the world.